Heads of Canadian banks continue to invest in oil & gas; claim its part of the green ‘transition’

“If some companies and industries fail to adjust to this new world, they will fail to exist.”

Mark Carney’s words were directed at central banks around the world, and the largest individual banks, warning that an unprecedented transfer of capital — trillions of dollars — by the globe’s most powerful institutions is the only way for them to save themselves.

Carney’s 2021 book, Value(s): Building A Better World For All, introduced the former central banker’s altruistic ambitions.

The very banks he influenced for decades, Carney told us, have to fundamentally shift the way they use the trillions of dollars under their control.

While the former governor of the Bank of Canada has been criticized for allowing banks to greenwash all of us by paying lip service to financial industry net-zero goals, he maintains that investments to expand pipelines, natural gas projects and new oil exploration will only hurt the institutions that fund these dirty energy deals.

His advice should worry millions of Canadian investors — everyday people with mutual funds in their registered retirement plans, equity in the company they work as a teller for or multiple bank stocks in their portfolio; the people who own the country’s big banks, which are led by men who continue to pay lip-service to the climate crisis.

The evidence is undeniable. Continued investments in projects such as pipelines, tar sands extraction and natural gas directly linked to dirty emissions make Canada’s banks among the worst actors in the global financial system.

The refusal of their leaders to align with the values of a growing number of Canadians, not only creates the moral mismatch Carney describes in his book, it puts more and more of us at financial risk. We simply cannot afford to live in a country whose system of monetary exchange is led by men who utterly fail to understand what’s at stake, as trillions of dollars stand to be made by sophisticated competitors literally fueling the green energy revolution, while Bay Street plays in the tar sands.

With each damning report on the amount of money big banks pour into the oil and gas industry, Canadians are becoming increasingly concerned about the financing of the climate crisis.

A peer reviewed study published in the journal of Environmental Research Letters found that 37 percent of the area burned across Canada and the United States from forest fires between 1986 and 2021 could be traced directly to 88 major fossil fuel companies and cement manufacturers. By continuing to finance these corporations, Canada’s major banks are quite literally adding fuel to the fire.

On June 13, the CEOs of Canada’s five largest banks — RBC, CIBC, TD, Scotiabank and BMO — were summoned to testify at the House of Commons Standing Committee on the Environment and Sustainable Development about their activities in the oil and gas industry. The Committee is looking into climate impacts caused by the Canadian financial system. The work runs parallel to the Senate's study of the Climate Aligned Finance Act.

But, despite hard lined questions from many of the members of the committee — which is made up of six Liberal MPs, four Conservatives, one from the Bloc Quebecois and one NDP MP, with an additional Liberal member present — the top bankers who sat in the hot seat refused to take any responsibility for their role in financing scorching temperatures, deadly wildfires, sea-level rise, worsening air quality and all the other immediate threats to planetary health.

“Look at the context of RBC in the world. Look in the context of RBC as the largest bank in the country. Look at the context of where we've come from, as a country that energy has been very important to the economy and will continue to be very important to the economy as we make this complex transition. I think we're focused on the right things,” David McKay, CEO of RBC, told committee members, who have been listening to the same line for at least a decade.

Another CEO picked up where his colleague left off.

“We are a signatory to the Net-zero Banking Alliance, and we do voluntarily commit to reducing our finance emissions from our lending investment portfolios over time to align with pathways to net zero by 2050. What I would say is I'm very proud of the work that has been done today,” CEO of Scotiabank, Scott Thomson, added.

The theme continued.

Despite a general understanding that fossil fuels are the main driver of anthropogenic climate change, it took until COP28 in 2023 for oil, gas and coal production to be officially named and recognized as the culprit. But the eventual agreement still carved out a significant number of loopholes to allow oil and gas companies to continue to emit at high levels.

The Alberta Oil Sands are the largest contributor to Canada’s greenhouse gas emissions.

(Howl Arts Collective)

Without the $140 billion that the five major banks handed to Canadian oil companies in 2023, they would not be able to produce the more than 5.5 million barrels of oil per day extracted from the Earth.

While Canadians plead with banks to invest in alternative sources of energy, the CEOs illustrated the addiction their company’s have to oil industry profits.

“This is a 30-year journey,” McKay claimed, describing the “transition” in the oil and gas sector to reach net zero targets. “So we're on that way.”

NDP MP Matthew Green listened incredulously. “We do not have 30 years!”

In 2023, global energy related emissions increased 1.1 percent, reaching a new record high of 37.4 billion tonnes. The 1.1 percent increase is equivalent to 410 million tonnes which is equivalent to 60 percent of emissions from Canada in 2022. But under the Paris Agreement, Canada and 194 other signatories agreed to decrease global emissions 45 percent by 2030 and all the way to net zero by 2050.

The summer of 2023, meanwhile, was the hottest on record according to both meteorological data that has been kept since the late-1800s, and dendrochronological data that dates back over 2,000 years. The weather patterns now seen globally around the year are part of what scientists call a doomsday cycle.

Amid the reality we are all experiencing on a daily basis, all of the five major Canadian banks have signed net zero pledges. Countless governments (including our federal one) agencies, and companies have pledged the same targets, without any success.

According to the United Nations Environment Programme, current national climate plans – for all the signatories to the Paris Agreement combined – would lead to an increase of almost nine percent in global greenhouse gas emissions by 2030, compared to 2010 levels.

Banks play a powerful role in determining what a country can and cannot achieve.

“What has actually transpired is that we're working with our clients to help them reduce their emissions. We're helping finance that transition, we're making unprecedented commitments to investing in Canadian renewable energy, we're making unprecedented commitments and executing on investing in equity and new solutions,” McKay claimed. “We made an unprecedented first commitment to $500 billion in sustainable finance, which we've already financed $400 billion.”

When pressed on the details, and how much money RBC has put into the oil and gas sector compared to the ‘transition’, McKay claimed to not have the data available.

It left many wondering how the head of the country’s biggest bank could show up on Parliament Hill without the information he was asked to talk about.

“I can tell you we've made a $15 billion commitment to that transition,” he said. He was again pressed on how that compares to investments in oil and gas. “I don't have it on top of my head because it breaks down by different sectors, different countries, different reasons, different capabilities, so we can get that for you in our disclosures.”

Various reports from a consortium of environmental groups have pegged RBC as the largest financier of fossil fuels globally in 2022. In that same year, RBC was responsible for $42.5 billion in financing to the fossil fuel industry, greater than the GDP of 106 of the world’s nations in the same year.

When a member of the standing committee pointed out that RBC is the number one financier of the Alberta oil sands, McKay said, “I'm not even sure if that's accurate. But we will check that for you.”

He continued with more promises.

“We have 80 percent of our clients that have presented a transition plan to get to net zero. It's important that we do this in an orderly fashion and we risk the entire journey. We have to protect jobs along the way.”

RBC previously released a troubling data point that the emissions from its financing of oil and gas companies are equivalent to all of the cars and light duty trucks on the road in Canada each year. Scientists have stated these emissions need to be cut in half in the next six years to have any hope of meeting the targets agreed to in Paris.

McKay was asked how he is planning to help do this. “The journey that we're on is a complex journey,” he replied.

The previous week, CEOs and Presidents of five of Canada’s major oil and gas companies appeared as witnesses in front of the same committee.

The bank CEOs were asked about working with them. Darryl White, CEO of BMO, said “if a client came in, we would assess the risks of their proposal, all of the risks of their proposal, whether they be environmental credit, market risk, legal risk, and we would assess their proposal as we would any other, regardless of whether it was a carbon related proposal or not”.

Carbon capture technology is increasingly being pushed by oil and gas companies that claim to be green, but experts say it is just more lip service.

(Maxim Tolchinsky /Unsplash)

Victor Dodig, President and CEO of CIBC, who is widely considered to be more progressive than his peers, said CIBC pledges to work with its clients in various sectors to achieve not only net zero in 2050, but interim targets along the way.

“So far, there's more work to do. We've set those targets for 2030. I would say that, in most instances, we are ahead of plan with our clients. And we remain committed to that 2050 Net Zero goal.”

Bharat Masrani, CEO of TD, said, “We are a great believer in an orderly transition. And we have to do both. We have to support the oil and gas industry, the responsible oil and gas industry, too, as we go through this orderly transition. And at the same time, make sure we are providing the capital and the investment to move to a net zero world.”

The “transition” the CEOs repeatedly referred to is vastly different from the energy transition that international organizations and environmental groups are calling for. In the International Energy Agency’s net zero roadmap, global oil demand declines 75 per cent by 2050 and gas demand declines 55 per cent. But instead of weaning off fossil fuels, the Canadian financial sector continues to make significant investments in the sector.

A recent report by the group Banking on Climate Chaos revealed that in 2023, the big five banks invested $103.85 billion in fossil fuel projects and $1.2 trillion since 2015.

MPs described the Canadian financial sector as a major part of the climate problem.

“I respectfully disagree with your points,” McKay argued. “We are a big part of the solution. You see commitments we've made to transition financing… we're very clear on the emissions that are coming from our lending portfolio, we've made commitments to reduce those by 2030. And to net zero. We've made commitments to reduce clients.”

It was revealed that a complaint was filed against RBC to the Competition Bureau of Canada for allegedly misleading the public on how close the company is to meeting its climate commitments. The complainants labelled the company’s conduct as pure “greenwashing”. A ruling against it could force the bank to stop claiming it is in line with the Paris commitments.

“There was one complaint from an individual to the Competition Bureau, the Competition Bureau did a full review and we've not heard anything from that,” McKay responded.

(Investors for Paris Compliance)

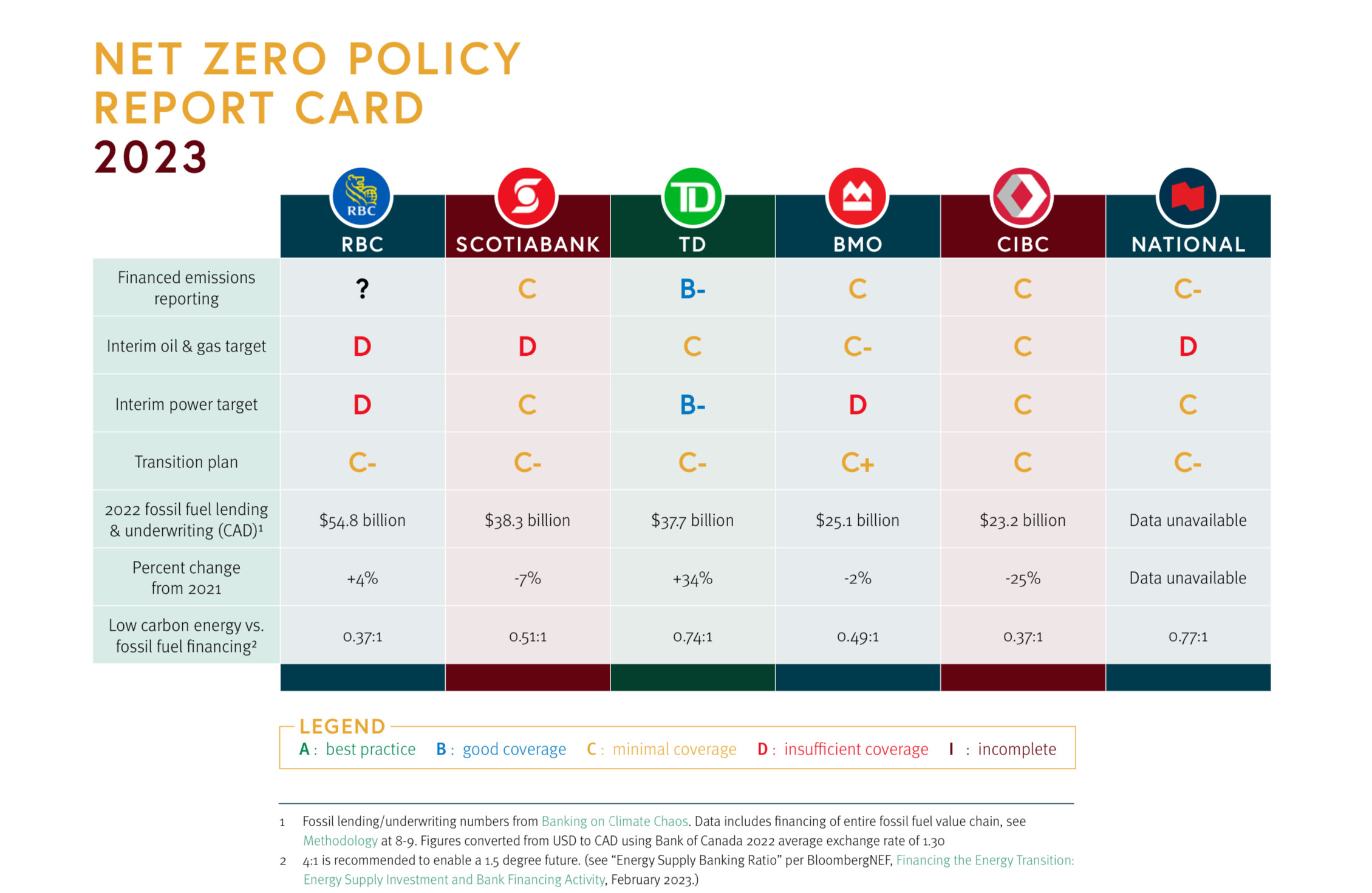

After committing to the Net Zero Banking Alliance in 2021, the organization Investors for Paris Compliance produced a report card for the six major Canadian banks — the five aforementioned plus National Bank — on a two-year progress update. The organizations used the financial institutions’ own summary reports to grade the banks and the only one that received anything above a C+ was TD which received two marks of B-, but it also undertook the greatest increase in fossil fuel lending and underwriting between 2021 and 2022, climbing 34 percent — RBC increased four percent and Scotiabank, BMO and CIBC decreased seven percent, two percent and 25 percent respectively.

The report notes that while all six banks have implemented interim oil and gas emissions reductions targets, RBC and Scotiabank have continued to advocate for fossil fuel extraction in Canada and no institution has outwardly supported a clean climate policy.

The hearings were unprecedented and marked a potential turning point to force Canadian banks to compete with international players.

“While each of the Canadian banks have climate commitments, none of them have a commensurate plan of action,” Julie Segal, senior manager of climate finance at Environmental Defence, said in a press release following the hearings. “The investments they make are holding the country back from climate progress and, until now, there had been no signs they would be held to account. New rules are needed to ensure the banks start helping instead of hindering our climate progress.”

Email: [email protected]

Twitter: @rachelnadia_

At a time when vital public information is needed by everyone, The Pointer has taken down our paywall on all stories to ensure every resident of Brampton, Mississauga and Niagara has access to the facts. For those who are able, we encourage you to consider a subscription. This will help us report on important public interest issues the community needs to know about now more than ever. You can register for a 30-day free trial HERE. Thereafter, The Pointer will charge $10 a month and you can cancel any time right on the website. Thank you

Submit a correction about this story