Flooded wallets: How climate change is driving up insurance costs, shrinking coverage

After years of dismissing warnings from his own daughter, a NASA climate scientist says her conservative father only accepted the reality of climate change once one unlikely authority weighed in: the mighty insurance industry.

“The fact that every insurance company has climate scientists on staff and insurance companies are all pricing in climate risk; there is no financial incentive for them to do that if it wasn't real,” Dr. Kate Marvel said on a recent podcast.

If climate change were a hoax, insurers would simply undercut one another, offering cheaper coverage and dismissing long-term risk, Marvel explained. Instead, they are doing the opposite; quietly rewriting the rules of risk as extreme weather becomes more frequent, more destructive and more expensive.

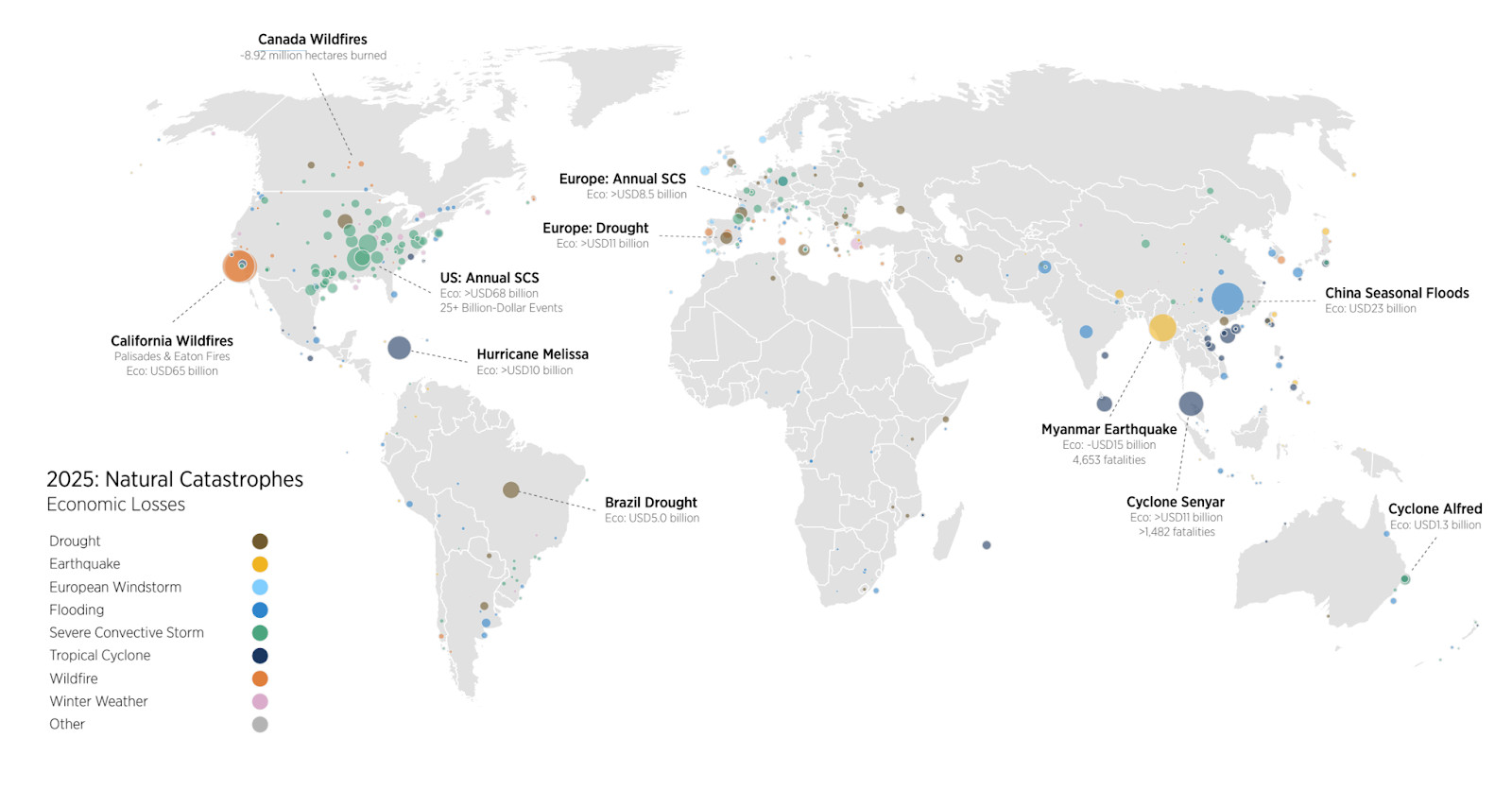

In 2025, the planet was battered by 55 billion-dollar weather catastrophes marked by the most expensive wildfire ever recorded, four catastrophic floods and storms, along with the sixth-deadliest heat wave in history, each of which took at least 1,000 lives.

The latest Natural Catastrophe and Climate Report from Gallagher Re finds that global direct economic losses from natural catastrophes in 2025 reached an estimated USD 296 billion, with insurers and public entities covering roughly USD 129 billion of that total, reflecting a growing trend of costly disasters driven by changing hazard conditions and socioeconomic exposure.

(Gallagher Re)

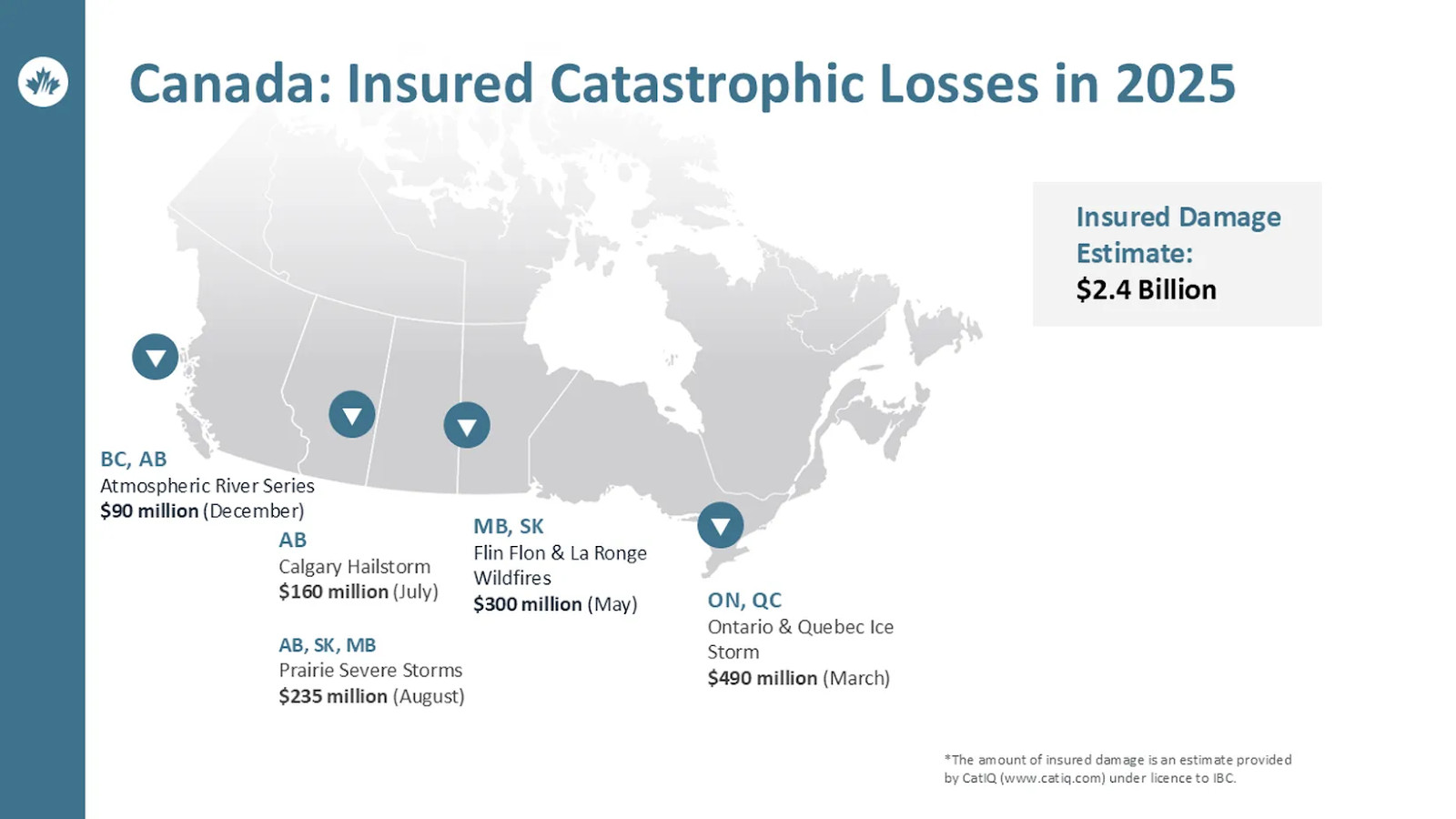

In Canada, insured losses from severe weather including ice storms, wildfires and flooding, exceeded $2.4 billion, according to Catastrophe Indices and Quantification Inc. (CatIQ).

This made 2025 the tenth costliest year on record for severe weather-related insured losses in Canada.

The latest report by the Insurance Bureau of Canada (IBC) shows that insured damage from severe weather events exceeded $2.4 billion in 2025, with Ontario recording the highest losses at $490 million.

(TOP: Insurance Bureau of Canada, BELOW: Gallagher Re)

Last year’s late-March ice storm in Ontario and Quebec contributed heavily to losses ($490 million) but this year, Ontario experienced a record-breaking winter storm earlier. On January 25, a storm dumped more than 60 centimetres of snow in parts of the Greater Toronto Area with Toronto Pearson Airport recording its snowiest day in 88 years with 46.2 centimetres, though the insured losses are still unknown.

But 2024 remains historic, with insured damage reaching a record $9.4 billion (12 times the annual average from 2001 to 2010), the costliest year in Canadian history for severe weather losses.

Much of that cost is ultimately passed on to homeowners through higher premiums, reduced coverage or outright exclusions.

In the Region of Peel, many areas in Mississauga, like Lisgar, Applewood Acres and Rathwood where residents say “flooding has become a way of life”, have borne the brunt, with insurance providers reportedly cancelling flood coverage, leaving homeowners fully responsible for any future flood damage.

Ward 3 Rathwood neighbourhood resident Karri Siemms says her home has flooded three times, once in 2013 and twice in 2024.

“Our home insurance premiums are now double what they should be for a comparable property,” Siemms told The Pointer.

“We pay nearly $300 per month for home insurance alone. Despite being with the same insurance company for 25 years, we received no meaningful support during the two flooding events in 2024, and neither claim was paid out.”

For her family, switching insurers is unfortunately not an option.

“Other insurance companies will not even provide a quote. The moment they see two flood claims — even unpaid ones — combined with the fact that our street has been flagged, the response is an automatic no,” she said.

“I thought home insurance was a regulated industry, yet homeowners like us have no transparency, no recourse, and no accountability. Customer service is poor, information is difficult to obtain, and decisions that have life-altering financial consequences are made behind closed doors.”

Siemms says this issue extends far beyond individual households, affecting property values, financial stability and the long-term viability of entire neighbourhoods.

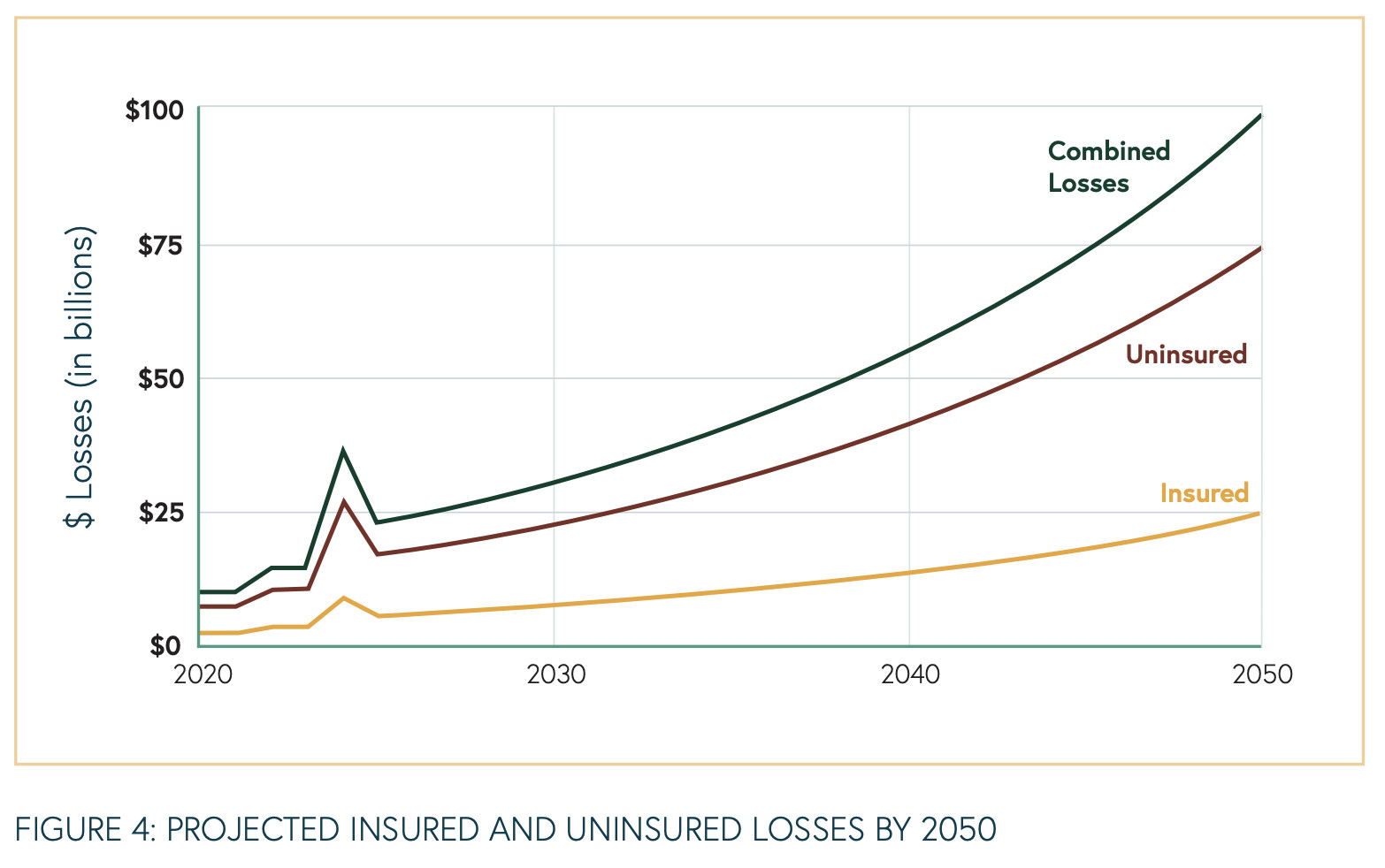

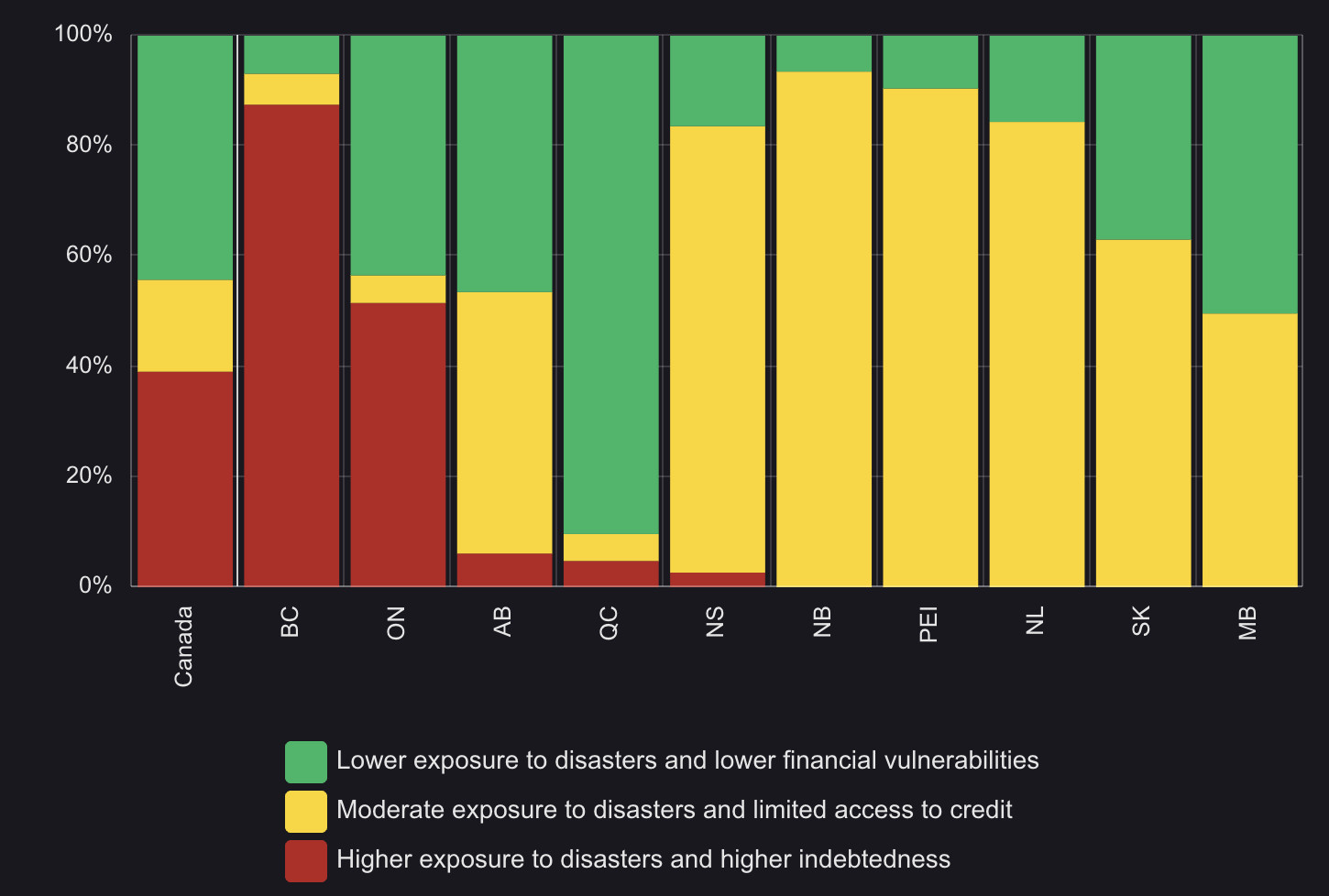

The bad news for many families like hers is that combined insured and uninsured climate damages in Canada could reach $100 billion per year by 2050, a new report by Investors for Paris Compliance suggests.

Swiss insurance company SwissRe projects natural catastrophes to grow five to seven percent annually, and Investors for Paris Compliance used a six percent midpoint to project 25 years of Canadian losses, averaging $5.44 billion in insured losses (2022-2024) with uninsured losses about three times higher.

(Investors for Paris Compliance)

“Over the last five years, Canadians have come to understand that extreme weather events are being driven by climate change,” Dr. Blair Feltmate, Head, Intact Centre on Climate Adaptation, told The Pointer.

“You can’t say any particular storm is caused by climate change but you can say the increasing number and magnitude of events is.”

Feltmate likens the trend to a baseball player suddenly hitting five times as many home runs after taking steroids.

“You can’t attribute any single home run to the steroids. But when the numbers jump that dramatically, cause and effect is pretty clear,” he explained.

From 1983 to 2008, catastrophic insurable losses in Canada averaged $250 million to $450 million annually, adjusted for inflation, a 2022 INTACT report stated. Since 2009, losses have exceeded $1 billion every year in 16 of the past 17 years, averaging nearly $3 billion annually and climbing along a steep curve.

“Things aren’t just getting worse, they’re getting worse faster,” Feltmate said.

Wildfires have emerged as a defining national challenge, with 2025 ranking second only to the record-setting 2023 for land burned (more than 8.9 million hectares) driving cascading impacts on public health, forestry, tourism and air quality across Canada and the U.S.

However, residential basement flooding is the largest climate-related cost facing Canadians, with insured losses roughly tripling over the past decade, Stéphane Tardif, Managing Director of Climate Risk at the Office of the Superintendent of Financial Institutions Canada, noted in a recent report.

“There is no part of Canada that’s immune to flooding from Halifax to Victoria to further north…in cities, in suburban or rural areas, it can pretty much strike anywhere,” Feltmate added.

Basement flooding has become a headache from coast to coast to coast in Canada, with many turning to Reddit for advice and tips on how to deal with it as well as the fluctuating insurance rates and coverage.

(Reddit)

Roughly 10 percent (1.5 million) of Canadian homes are now no longer eligible for flood insurance while coverage caps for basement flooding have also fallen sharply. The cost of repairing a flooded basement can range between $43,000 to over $50,000, a financial shock that can render homes uninhabitable within days if coverage is limited or denied.

This adds extra pressure to household wallets, mainly in British Columbia and Ontario.

“Households that are both financially vulnerable and exposed to natural disasters hold a large fraction of household debt,” a 2021 Bank of Canada report emphasized. “That’s a predictable financial risk hiding in plain sight. We don’t need sophisticated modelling to know extreme weather costs will keep rising,” Investors for Paris Compliance, Senior Analyst, Kiera Taylor, said.

The Bank of Canada previously reported nearly 39 percent of Canadian household debt (just under two-fifths) is held in areas where families are both heavily in debt and vulnerable to natural disasters.

Yet while insurers are adjusting to climate reality, critics say the financial burden is increasingly falling on households, not the industries most responsible for driving climate change in the first place.

“Canadians are getting hit twice,” Investors for Paris Compliance, Senior Analyst, Kiera Taylor, told The Pointer.

First, households face rising premiums and shrinking coverage. Then, they pay again through public spending on disaster response, adaptation and recovery.

“The insurance industry’s plan right now is to continue raising rates while asking governments to spend more on adaptation and resilience. That shifts the liability onto typical Canadians, both as policyholders and as taxpayers,” Taylor noted.

She believes this trajectory is unjust, particularly given that major corporate emitters continue to profit while climate damages accelerate.

“There are actors that are profiting from the acceleration of climate change while imposing public harms, and there are mechanisms to recover those costs,” she added.

There have been advances in attribution science, which is research that links emissions from specific companies to measurable climate damages, opening new pathways for cost recovery.

In a September study, researchers found emissions from any of the 14 biggest carbon majors including ExxonMobil and Saudi Aramco were sufficient to trigger more than 50 extreme heatwaves with global heating increasing the intensity of 213 major heatwaves from 2000 to 2023 by up to 2.2 degrees Celsius.

Using attribution analysis, scientists compared today’s hotter climate with a pre-industrial baseline, quantifying each company’s contribution and showing that emissions from fossil fuel production were responsible for roughly half of the added intensity.

Experts have pointed out these findings could become key evidence in legal efforts to hold polluters accountable, as courts increasingly recognize the link between corporate emissions and climate disasters.

Unfortunately, despite decades of knowledge and lobbying to protect profits, no major fossil fuel company has yet been held legally liable.

But attribution science might change that.

And Canada has already set a precedent, albeit in a different industry. In March last year, major tobacco companies including JTI-Macdonald Corp., Rothmans, Benson & Hedges and Imperial Tobacco Canada were forced to pay $32.5 billion after governments moved to recover public health costs.

“There’s no reason that same logic can’t apply to emissions and extreme weather damage,” Taylor said.

Globally, climate litigation is accelerating with courts in Germany, the United States and Europe increasingly recognizing that major emitters can, in principle, be held liable for climate-related harms even when cases fail on narrow evidentiary grounds.

In July 2025, the International Court of Justice (ICJ) also issued a landmark advisory opinion confirming that nations have binding legal obligations under international law to prevent significant climate harm, safeguard human rights from climate impacts and cooperate on climate action.

The ICJ noted that inaction, such as approving new fossil fuel projects, can amount to an “internationally wrongful act” with duties of cessation and reparation, setting a new standard of “highest possible ambition” for major emitters and creating pathways for climate litigation.

In Canada, Taylor argues, provinces and Ottawa could get ahead of inevitable litigation by introducing cost-recovery legislation aimed at major emitters including fossil fuel companies.

“In Ontario, the province bears the cost of emergency responses to catastrophes like wildfires and floods, and the federal government often steps in to help cover these recovery costs,” Taylor noted.

“Cost recovery is already an inevitable trend globally. The question is whether provinces and the federal government will proactively facilitate cost recovery rather than letting it play out through messy litigation. Either way, I believe it’s coming to Canada.”

While that remains to be seen, the youth in Canada have already taken charge by holding their governments accountable in court.

In Mathur v. Ontario, seven activists are challenging the Doug Ford government over weakened climate targets. In La Rose v. Canada, 15 young Canadians are suing the federal government for actions contributing to climate change. Both cases share a common foundation: the youths argue that the actions, or lack thereof, by provincial and federal leaders violate their Charter rights to life, liberty and security.

As the accountability debates unfold, critics have observed that Canada already knows how to significantly reduce climate risk; it just isn’t moving fast enough.

“We are policy-rich and operations-poor,” Feltmate said.

“Strategies come out, everyone’s pleased and six months later they’re sitting on a shelf.”

In 2023, Ottawa launched the National Adaptation Strategy, focused on flooding, wildfire and extreme heat, with multiple targets set to be met by 2040.

A 2025 audit by Environment Commissioner Jerry DeMarco found the strategy “was not effectively designed” and failed to prioritize Canada’s most pressing climate risks.

The report concluded it does not clearly define expected results, timelines, or accountabilities and only one of its three core components has been implemented since its launch, despite $1.6 billion being committed to the plan.

One of the components hit the most was health and climate change.

DeMarco noted that while risks such as wildfire smoke and the rapid spread of Lyme disease were identified during consultations, they were excluded from final targets. Short-term health impacts from wildfire smoke alone were estimated to cost between $410 million and $1.8 billion annually, but there were still “no dedicated targets” to address these issues.

Since 2015, the federal government has invested roughly $160 billion in cutting greenhouse-gas emissions. Over the same period, only $6.6 billion went toward adaptation, according to the Government of Canada.

Feltmate calls this a 24-to-1 imbalance.

“For every $1 they put in adaptation, they put $24 in mitigation. It's a completely lopsided commitment,” he said.

“They need to put far more money into adaptation while still working to mitigate greenhouse gas emissions.”

Ironically, “municipalities are moving adaptation forward faster than provinces or the federal government”, driven by practical necessity rather than ideology.

One example is the City of Mississauga, a municipality that has had one of the worst flooding problems in the Greater Toronto Area, which has invested between $231.5 million and $265 million since 2016 in stormwater infrastructure and climate adaptation measures. An additional $308 million to $342.5 million is planned for the next decade.

Linda Blakely, a member of the Flood Committee for Applewood Acres, said residents have been campaigning for the city to expedite flood-mitigation efforts following the two once-in-a-century storms.

“Most of my neighbours had huge increases and/or got denied coverage by their insurer after the July and Aug. 2024 floods,” Blakely told The Pointer.

Mayor Carolyn Parrish has frequently criticized the lack of support from Ottawa and Queen’s Park, overlooking the city like the “poor cousin”.

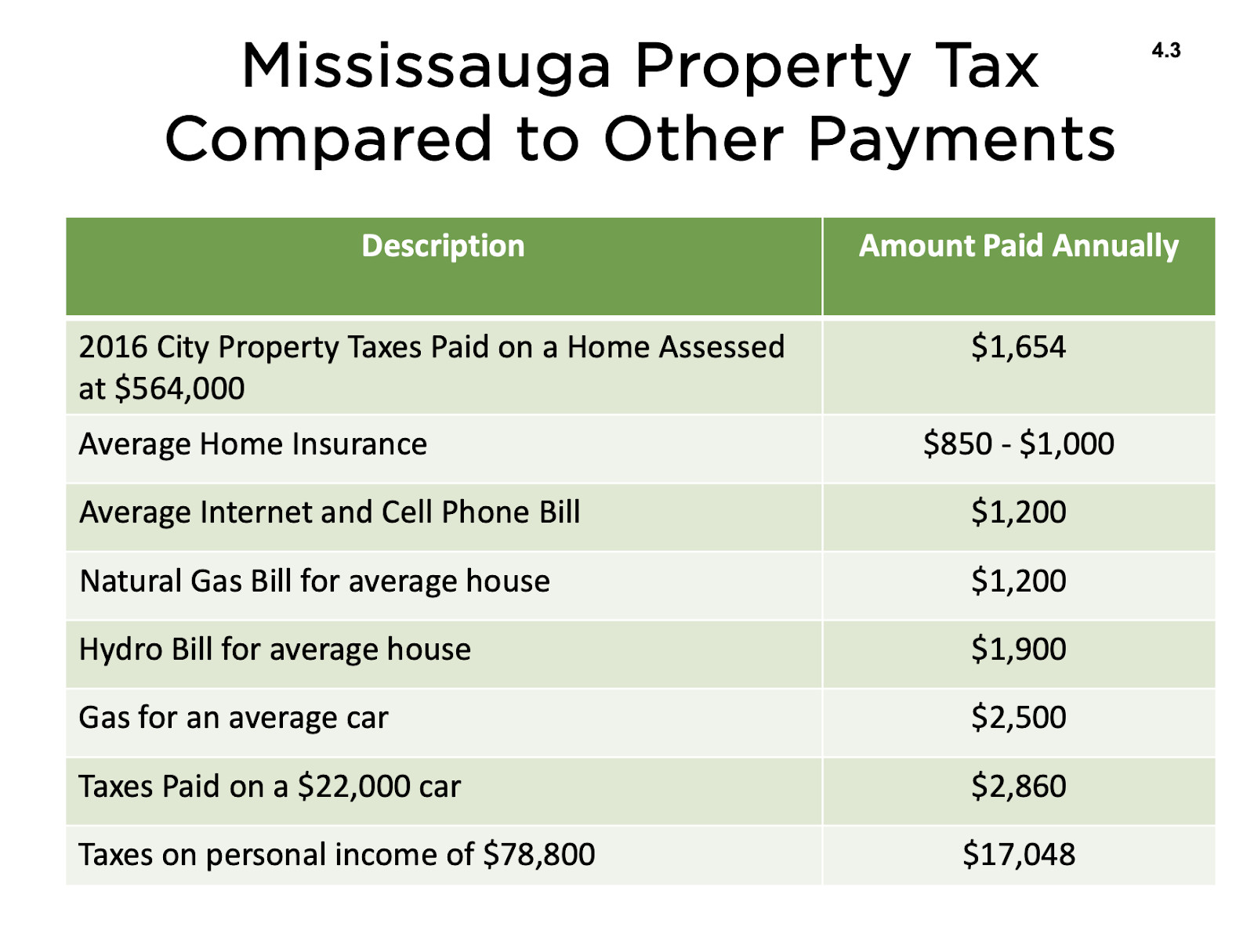

The average home insurance premium in Mississauga was between $850 and $1,000 in 2016-17. As of 2026, the estimated average has risen to $1,782 per year or about $149 per month, according to Rates.ca Home Insuramap data.

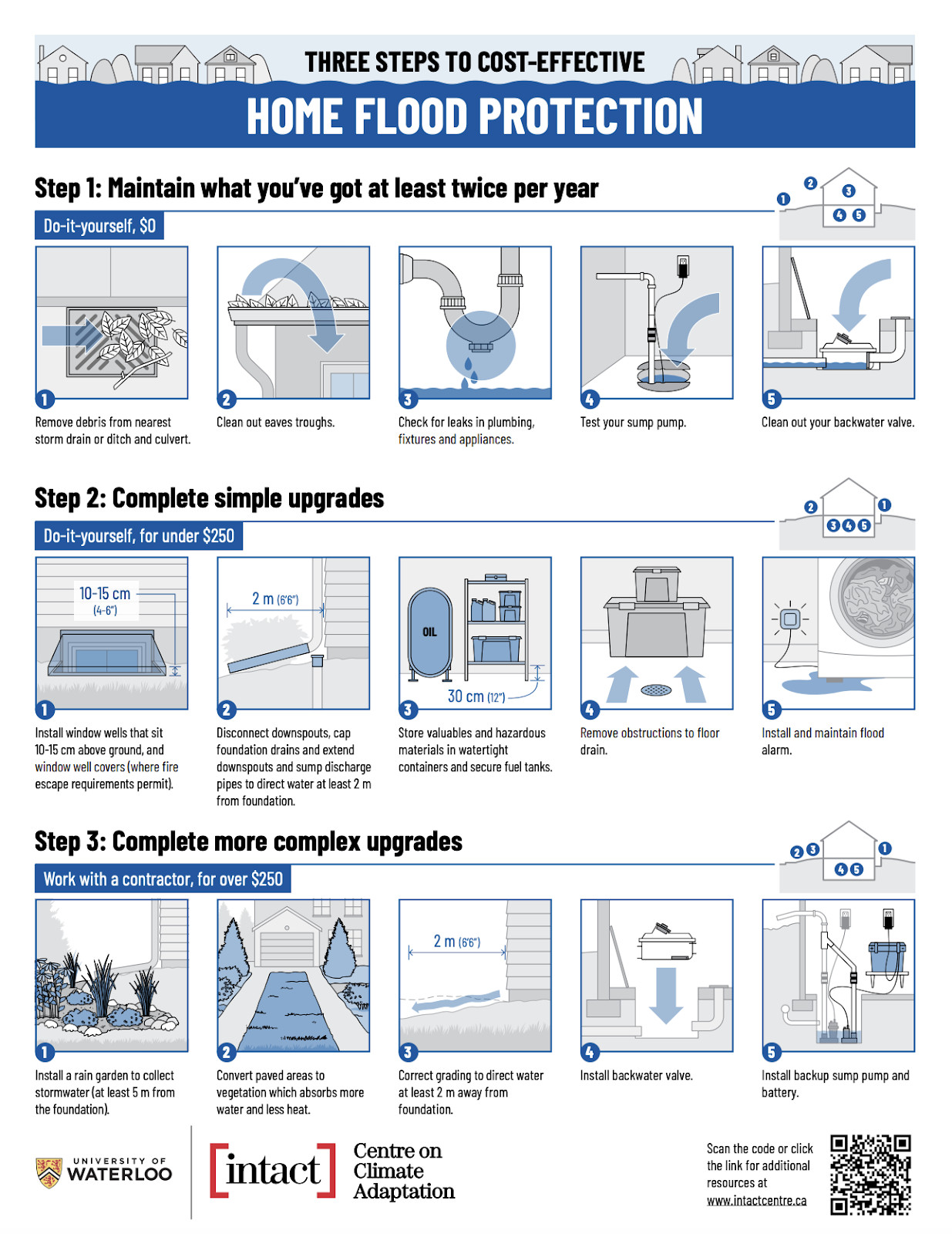

Feltmate, who has experienced flooding in one of his own investment properties, stresses that there are steps homeowners can take to prepare their homes before the dark clouds take over.

Simple actions like checking that sump pumps are working, installing plastic covers over window wells, redirecting downspouts away from foundations, and ensuring proper grading around the house, can dramatically reduce flood risk, sometimes cutting vulnerability from high to moderate in just a weekend.

Dr. Blair Feltmate, Head, Intact Centre on Climate Adaptation, says clear, visual guidance like one-page infographics distributed by insurers, municipalities or banks can make it easy for people to know exactly what steps to take. Feltman has observed 70 percent of homeowners act on these recommendations within six months, reducing potential flood damage.

(INTACT)

For a slightly higher investment, he recommends adding battery backups for sump pumps or other protective equipment to ensure these systems work during power outages.

“People act when they know what to do. The problem is they’re not being mobilized at scale,” Feltmate said.

For Dr. Marvel’s father, it was the insurance industry that finally cut through climate skepticism. For millions of Canadians now watching premiums rise and coverage shrink, that same financial reality may be impossible to ignore.

The question is whether governments at both the provincial and federal level will act quickly enough not just to adapt to a warming climate but to confront who pays for the damage when they don’t.

Email: [email protected]

At a time when vital public information is needed by everyone, The Pointer has taken down our paywall on all stories to ensure every resident of Brampton, Mississauga and Niagara has access to the facts. For those who are able, we encourage you to consider a subscription. This will help us report on important public interest issues the community needs to know about now more than ever. You can register for a 30-day free trial HERE. Thereafter, The Pointer will charge $10 a month and you can cancel any time right on the website. Thank you

Submit a correction about this story