The climate crisis might jeopardize your retirement: Experts warn Canada’s pension watchdog is underestimating risks

Wildfires, floods and other severe weather events are not going away, they are only becoming more common, part of what scientists have been warning for decades. The economic shocks of changing oceans, the jet stream and the loss of our polar ice caps, as well as mass glacial loss in Canada turning our forests into tinder boxes, will only get worse as global temperatures blow past the tipping point that marked severe planetary distress.

For those who have to plan around the financial reality of climate change, short and long-term economic forecasts may be too optimistic, leaving younger Canadians particularly exposed to a future where pension plans and other investments for retirement may not be nearly as safe as they once seemed.

What happens to retirement planning for millions of Canadians if climate change melts away not just ice sheets, but also their financial future?

That question is at the heart of a growing difference of opinion over how Canada’s pension infrastructure should be safeguarded from the single largest system-risk to the global economy ever seen.

Environmental lawyers and advocates warn that the federal office responsible for protecting the future of the Canada Pension Plan (CPP) is failing to account for the bewildering financial risks of global warming—the World Economic Forum projects $17.3 trillion (CAD) in economic losses over the next 25 years due to climate change—leaving millions of nest eggs exposed.

On August 28, Ecojustice, on behalf of advocacy group Shift: Action for Pension Wealth and Planet Health, sent a letter to Chief Actuary Assia Billig, accusing the Office of the Chief Actuary (OCA) of dangerously underplaying the financial risks climate change poses to the Canada Pension Plan (CPP) and the Public Sector Pension Plan (PSPP).

Combined, those funds support the retirement of more than 22 million Canadians who pay into the plan with a promise of financial security; a safety net designed to help them walk comfortably without fear of falling into a financial abyss during their old age, no matter how hard the markets sway.

“Failing to assess and report credibly on the scope of climate-related financial risks could have reverberating and detrimental impacts on the financial sustainability of plans and programs,” the letter warned.

In May, the CPP investment annual report boasted assets of $714.4 billion, strong yearly returns of 9.3 percent, and projections to surpass $1 trillion by 2031.

Chief Executive Officer John Graham reassured contributors that the plan “remains financially sustainable for at least the next 75 years,” thanks in part to its three-year audit by the OCA.

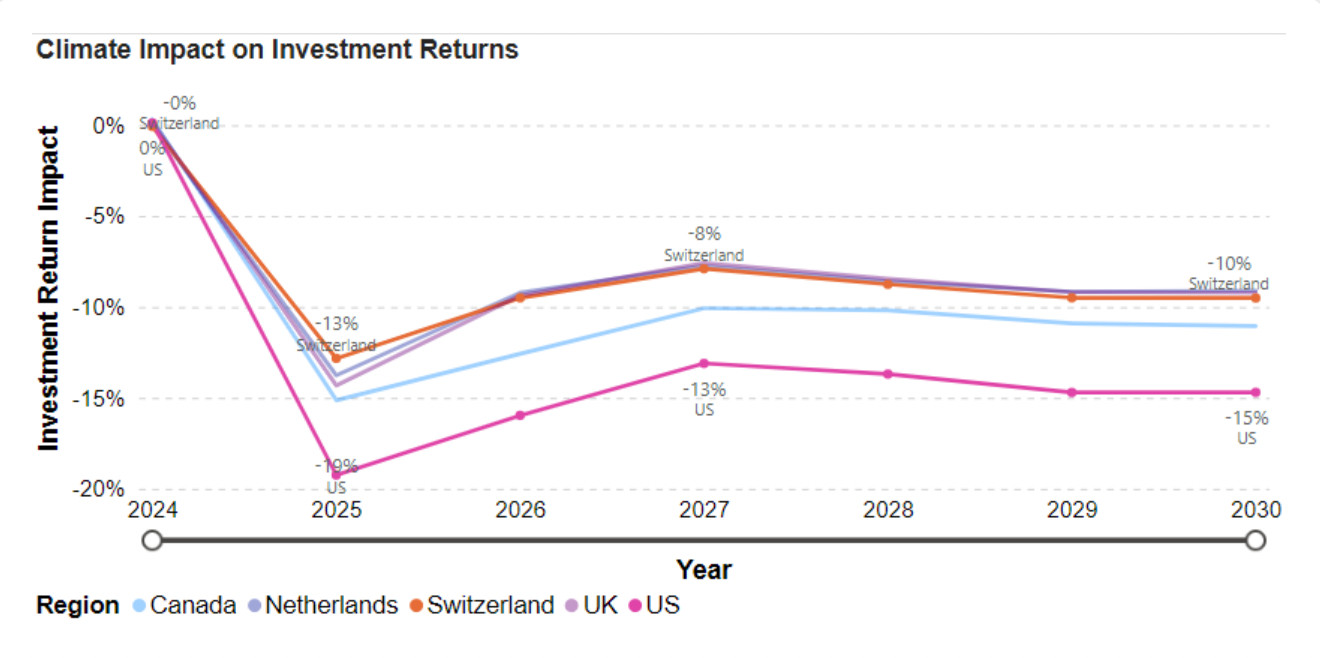

In a November 2024 report, Ortec Finance examined the climate risk exposure of five major pension systems, including those in the U.S. and Canada, and warned that North American pension funds could see a drop of 50 percent or more in investment returns by 2040 if global temperatures rise by 3.7 degrees Celsius under a business-as-usual scenario.

(Climate risks facing the pension industry worldwide/Ortec Finance)

For Adam Scott, executive director of Shift, who has spent years analyzing how pension funds address the risks of climate change, that kind of reassurance was more troubling than comforting.

“They (CPP) bragged about OCA report giving them a clean bill of health on the future…we thought, that doesn’t make any sense. Sure, they can reach that conclusion based on demographics and contributions. But it’s not possible to make that statement without considering (the) climate,” Scott told The Pointer.

“This is something that’s often missed in Canadian discussions about climate change. People don’t fully grasp what the consequences of inaction could be. And especially in the financial sector, we keep seeing a low level of literacy around the realities of climate science.”

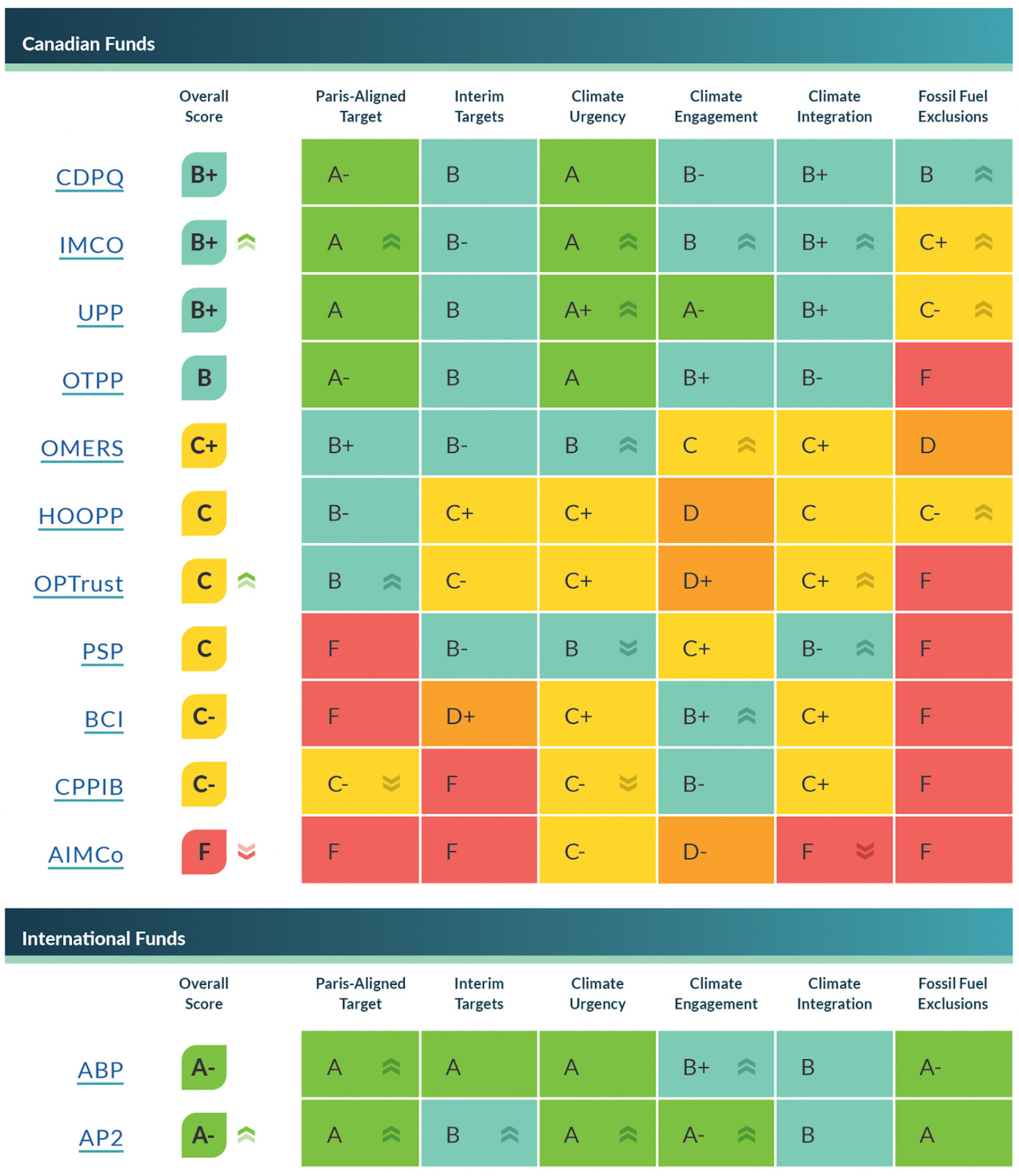

In February, Shift released its Canadian Pension Climate Report, evaluating the climate policies of 11 of Canada’s largest pension funds, which together manage $2.4 trillion in retirement savings. In nearly every case, Scott argues, Canada’s fund managers are drastically underestimating the financial shocks that runaway global warming could unleash.

The 2024 Canadian Pension Climate Report Card evaluates how funds are managing climate-related risks using six key indicators, such as Paris-aligned targets, climate engagement, and fossil fuel exclusions, and highlights that while many funds recognize these risks, most Canadian funds fail to effectively exclude fossil fuel investments, and urgent action is needed to ensure they can meet their long-term obligations to beneficiaries.

(2024 Canadian Pension Climate Report Card/Shift)

In the CPP’s case, Scott points to its use of limited scenario analyses that attempt to predict what might happen under different levels of warming. According to the fund’s own models, even under a catastrophic three degrees Celsius warming scenario, the portfolio would only lose four percent in value.

“That’s nonsensical. It shows they haven’t understood how to do the analysis properly. They’re not looking at the systemic risks across the economy,” he said.

In their letter, Shift and Ecojustice outline several major shortcomings in the OCA’s recent analysis, including failure to properly account for physical risks such as tipping points; cascading ecological failures, and extreme weather events; and reliance on outdated models that underestimated global Gross Domestic Product (GDP) losses in high-warming scenarios.

The letter also criticizes the OCA for lacking qualitative analysis that could better communicate uncertainty and systemic risks to the public, and for ignoring the potential of fossil fuel investments to become stranded assets as the world moves away from carbon-intensive energy.

The organizations assert that the OCA’s “baseline” scenario assumptions were overly optimistic, failing to factor in the climate impacts already locked into the global system.

Scott says omitting or minimizing climate risks from these assessments may give Canadians a false sense of security and set them up for painful surprises in the decades ahead.

The danger is not simply that climate disasters might hurt a few assets; it’s that they could destabilize entire systems—trade, infrastructure, agriculture, public health, and finance, simultaneously.

“Most of the growth of a pension fund comes from the growth of the overall economy. If the global economy shrinks because of climate chaos, pensions shrink with it,” he explained.

Ecojustice lawyer Tanya Jemec says the OCA holds more than just a technical responsibility.

“The Chief Actuary has a really important role…a professional responsibility, to fully assess and report on climate-related financial risks. Its reports inform government policy and highlight risks that affect millions of Canadians. To understate climate risks is to miss the true financial impacts that science is warning us about,” Jemec told The Pointer.

In the UK, the Institute and Faculty of Actuaries, in collaboration with climate scientists at the University of Exeter, is leading the way in climate-scenario modelling within financial services.

“There is a disconnect between climate science and the economic models that underpin financial services climate-scenario modelling, where model parsimony has cost us real-world efficacy,” a July 2023 report noted.

“Real-world impacts of climate change, such as the impact of tipping points (both positive and negative, transition and physical-risk related), sea-level rise and involuntary mass migration, are largely excluded from the damage functions of public reference climate-change economic models.”

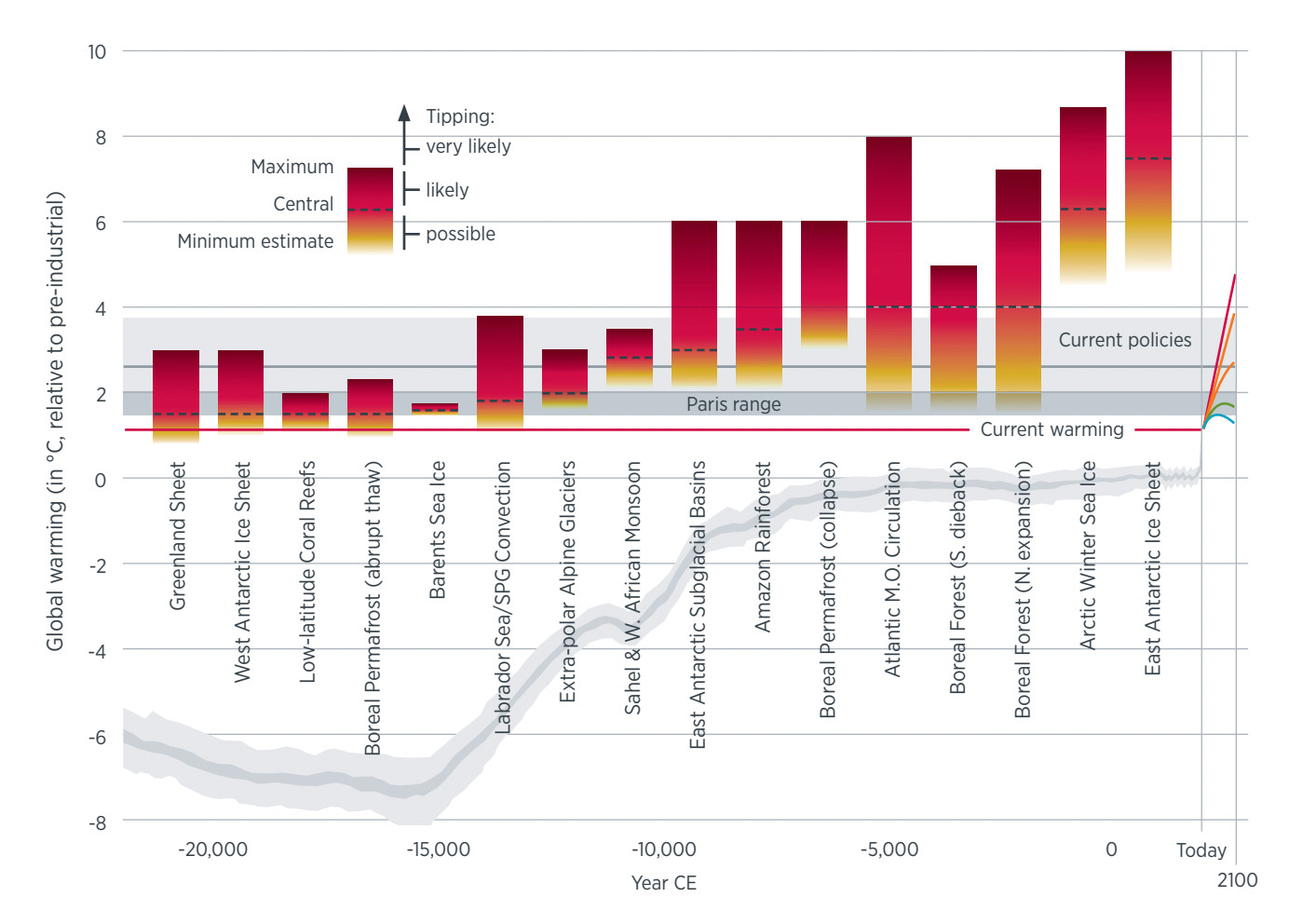

As global temperatures exceed 1.5 degrees Celsius, scientists warn that critical climate "tipping points" like ice sheet collapse and Amazon dieback could trigger irreversible changes, accelerating global warming and worsening impacts such as sea-level rise.

(The Emperor’s New Climate Scenarios report)

The report also highlights that some models unrealistically show a positive economic outcome in a high-emissions world, whereas others predict a 65 percent GDP loss or a 50 to 60 percent decline in existing financial assets if climate change is not mitigated, with these projections likely being conservative.

Jemec notes that the UK’s approach focuses on not just quantitative data, but also qualitative scenarios to better capture uncertainties and real-world impacts; something that’s lacking here in Canada, and one they are advocating for in the letter to the OCA.

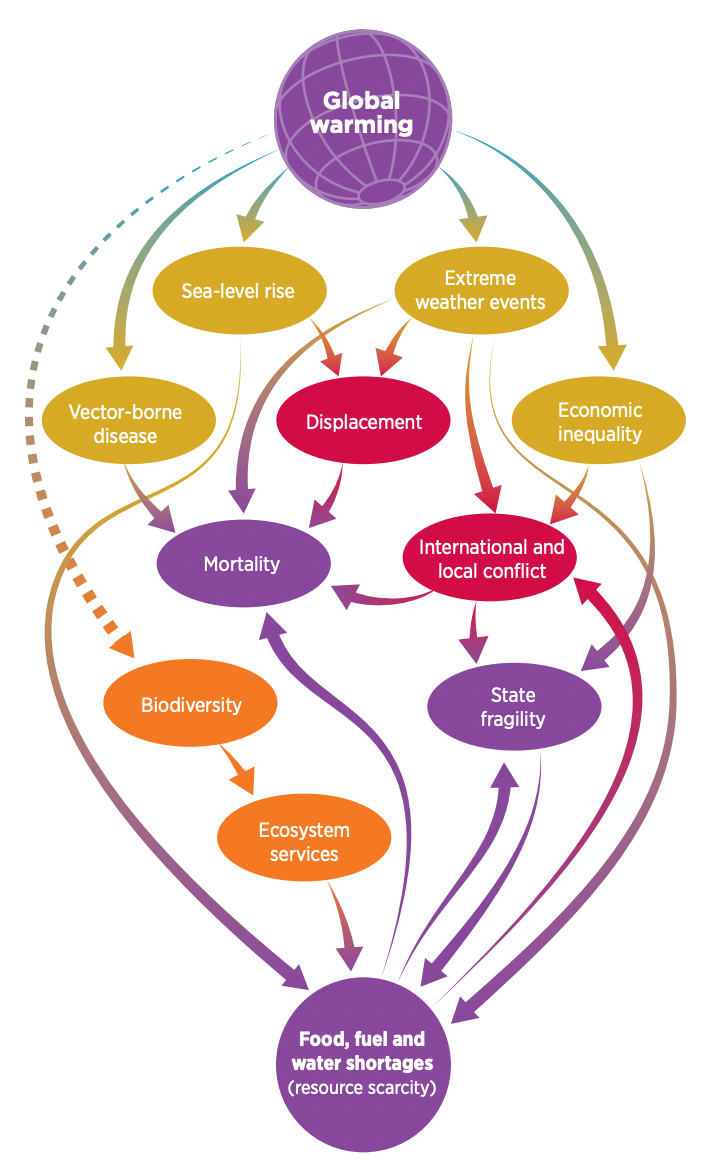

Global warming is projected to trigger a range of interconnected risk factors, which will, in turn, affect financial markets and the solvency of financial institutions. In response, experts have been urging firms to develop qualitative climate scenarios to explore how these cascading risks could unfold and identify possible mitigation strategies. Visual tools, such as flood maps, can help illustrate the stark differences between areas that would be impacted under a 1.5 degrees Celsius scenario compared to a more extreme four degrees Celsius scenario.

(The Emperor’s New Climate Scenarios report)

Part of the challenge is the financial sector’s discomfort with uncertainty.

“There’s a desire to have a quantitative fixed number that can be assessed. But climate change is unprecedented. The trajectory is clear: more warming means destabilized natural and economic systems. But you can’t boil that down to a single number with certainty. That doesn’t mean you ignore it. It means you need to communicate it differently,” she explained.

Until this year, many Canadians viewed wildfires as a problem limited to the northern and western regions of the country. That perception changed dramatically in August 2024 when the Kawartha Lakes wildfires in Ontario made it clear that these devastating fires are not just a rural forest issue.

The 2023 Canadian wildfires were the worst on record in at least 20 years, burning millions of hectares of forest and sending massive plumes of smoke across North America and even reaching Europe. This smoke filled the air with tiny, harmful particles (PM2.5), making air quality unsafe in many regions. A recent study notes, in Canada and the U.S., people experienced spikes in pollution that sometimes exceeded health guidelines, and overall, around 354 million people in North America and Europe were exposed to this smoke. Scientists estimate that thousands of people died from short-term exposure, and tens of thousands suffered long-term health impacts.

(Nature)

The Summer 2024 record rainfall across southwestern Ontario, including the Greater Toronto Area (GTA), caused widespread flooding that severely affected farms and fields.

In 2023, Ontario’s Provincial Climate Change Impact Assessment warned that the future looked grim for the province’s agriculture: By the 2050s, certain crops like apples may no longer be viable in the province. By the 2080s, prolonged heatwaves could decimate up to a quarter of the province’s livestock.

Even something as simple as Canada’s beloved morning coffee has been hit hard by climate change, with global disruptions in coffee-producing regions impacting daily routines and driving up costs.

In 2023-24, severe droughts in key coffee-producing regions, particularly Brazil and Vietnam, devastated harvests, causing global coffee prices to spike.

As a major importer of coffee from these regions, Canada felt the strain, with retail prices for roasted and ground coffee climbing by 20.7 percent in June 2022. More recently, in August 2023, the price of roasted and ground coffee rose by another 9.2 percent year over year, according to Statistics Canada.

The Insurance Bureau of Canada (IBC) says climate change influences more and bigger floods, wildfires, hailstorms, and windstorms, which are costing billions and putting people and property at risk.

In 2024, insurers paid out over $9 billion, surpassing the previous record set in 2016 by more than $2 billion.

The flash flooding in the Greater Toronto Area (GTA) alone led to nearly $1 billion in insured losses, affecting homes, businesses, and vehicles.

This surge in climate-related events has driven up insurance premiums and left many homeowners with shrinking coverage, particularly in flood-prone areas.

In 2024, home insurance premiums in Ontario rose by 84 percent between 2014 and 2024, with a 12.7 percent increase in 2024 and a further 5.7 percent jump in 2025, with some residents struggling to secure coverage at all.

Insurers are predicting further double-digit growth.

In July, Investors for Paris Compliance (I4PC) sent a letter to Ontario’s Financial Services Regulatory Authority (FSRA), urging the government to demand greater transparency from insurers, particularly on how premiums are determined and how climate risks are priced.

Experts note that insurers fail to provide sufficient public analysis, leaving residents with unaffordable premiums and limited protection.

Worse still, some insurers continue to invest in fossil fuels, exacerbating the very climate risks they are supposed to mitigate.

This issue extends beyond insurers, as CPP Investments and PSP remain heavily exposed to fossil fuels, the very industry many believe is driving the climate risks it aims to mitigate.

“Both the CPP and PSP have continued to invest in companies that, if we're successful in addressing climate change, would not be viable long-term…They are betting against the transition to a sustainable future with many of their investment decisions. Despite claims of being long-term investors, aiming to hold assets for over 10 years, these funds are investing in companies whose business models are fundamentally incompatible with climate goals,” Scott explained.

In 2024, a CPPIB spokesperson reported that 3.5 percent of its $647-billion portfolio, or $22.6 billion, was invested in fossil fuels.

Scott says this figure likely underestimates the true exposure, as it only accounts for oil, gas, and coal producers, excluding related infrastructure and utilities. Without more detailed disclosure from CPPIB, it's impossible to fully assess the extent of its fossil fuel investments, with Shift estimating the actual figure could be nearly double the disclosed amount of $22.6 billion.

On the other hand, PSP Investments holds an estimated $6.2 billion to $8.1 billion in fossil fuel assets as of March 31, 2024.

“These are companies whose business models are about expanding fossil fuel production and climate pollution,” Scott said.

“Pension funds say they’re long-term investors. But these companies have no long-term future in a successful climate transition. So not only is it a substantial financial risk, these investments actively make the climate crisis worse.”

CPP Investments, for its part, defends its strategy.

The fund has made high-profile investments in renewables and says it is reducing the carbon intensity of its portfolio. It emphasizes a “whole-economy transition” approach.

Still, even the CPP’s own report notes that its long-term assumptions are “subject to uncertainty and may not prove to be correct.” Critics say that disclaimer, buried deep in the technical appendices, contradicts the front-page message of long-term stability.

A renowned Canadian economist coined the term ‘Tragedy of the Horizons’ to explain how financial institutions’ short-term outlooks prevent them from adequately addressing the long-term risks of climate change. Among those risks is the potential for a “carbon bubble,” where fossil fuel assets are overvalued in anticipation of climate policies that could render them obsolete.

That man’s name is, Mark Carney.

Greenwashing and fossil fuel lobbyists have their claws so deep that, by August, they had secured 25 meetings with Carney since his victory in the Liberal Party leadership race in March, according to a recent Environmental Defence report.

That troubles environmental advocates and economic experts alike because the Canadian economy is already absorbing climate-related costs, from wildfire-related health expenses to heat damage to infrastructure.

It has led the Bank of Canada to think about climate change and its impact on financial systems.

“If climate change impacts the financial system at the end of the day, it's going to end up impacting Canadians and Canadians’ standard of living,” Bank of Canada senior policy director Erik Ens said.

A report from the Canadian Climate Institute warns that the economy could lose around $35 billion by 2030, and potentially hit $78 to $101 billion per year by 2050 in a high-impact scenario.

“When you look to the future, you see how these impacts threaten the stability of pension funds. Physical risks mean the investments that underlie pensions could underperform or even be wiped out,” Jemec says.

The core issue is timing, as actuarial models and pension plans are built on decades-long forecasts. If they are flawed now, there may be no opportunity to fix them before irreversible damage occurs.

“This sounds wonky, I know. But it’s simple: the climate crisis is going to hit your pocketbook. Acting now is the only way to protect pensions for future generations,” Scott said.

Both he and Jemec warn that younger Canadians, those under 40, who will begin collecting CPP after 2050, are “most at risk”.

“If you’re 25 today, there’s a real question of whether you’ll ever get the pension you’re promised. You may have to pay more, or get less. That’s how directly climate change impacts the mandate of these funds,” he noted.

Pensions, long regarded as a steady, secure, and dependable financial safety net, may be losing that reliability, and if Canada’s pension watchdog continues to downplay climate risk, the financial futures of millions could be in jeopardy.

“The lowest cost, smartest financial decision we can make is to act on climate as aggressively as possible. Anything else is a misreading of climate science, and a gamble with Canadians’ retirements,” Scott said.

Both Ecojustice and Shift confirmed to The Pointer that they have not received any response or acknowledgement from the OCA yet.

“The physical impacts of climate change can mean that the investments that underlie the security of the pension plan are put at severe risk, so the returns are lower than expected,” Jemec added; “or those investments can even be wiped out…the Office of the Chief Actuary (has) an opportunity, and in my opinion, an obligation to highlight the looming societal and financial risks of climate change.”

Email: [email protected]

At a time when vital public information is needed by everyone, The Pointer has taken down our paywall on all stories to ensure every resident of Brampton, Mississauga and Niagara has access to the facts. For those who are able, we encourage you to consider a subscription. This will help us report on important public interest issues the community needs to know about now more than ever. You can register for a 30-day free trial HERE. Thereafter, The Pointer will charge $10 a month and you can cancel any time right on the website. Thank you

Submit a correction about this story