COVID-19 worrying homeowners, renters and sellers in Peel

In Peel, people are being laid off from their jobs. Without the security of a regular pay cheque and amid skyhigh property and rental costs in Brampton and Mississauga, realtors, landlords and tenants face an uncertain future.

The first thing people usually budget for in their monthly expenses is rent and mortgage payments. Keeping a roof over one’s head is at the heart of most people’s financial planning.

But no one could have planned for this.

As municipal, provincial and federal leaders scramble to respond to the health and economic impacts of COVID-19, housing is the main financial fear for many. Since the outbreak, more than 925,000 people have signed onto employment insurance (EI), as layoffs continue across Canada.

A row of houses in Brampton, where little real estate activity is happening

Last week, a mortgage deferral program was announced by Canada’s major banks as an option to help people struggling with the impact of COVID-19. It was welcomed by leaders, who saw it as relief for the thousands who have found themselves suddenly out of work. However, closer scrutiny of the offer showed that interest would not be waived for the period of the deferral, with each request handled on a case-by-case basis. The program, heralded as a COVID-19 rescue package, was suspiciously similar to a mortgage deferral in normal economic conditions, and while Prime Minister Justin Trudeau issued a not so veiled directive to the big banks this week, telling them to offer relief on credit card debt, which could free up some money for individuals scrambling to cover housing costs, he did not address the banks’ lack of action on a more long-term solution for homeowners.

Banks are facing widespread exposure due to the crisis, and aren’t interested in dropping multi-year mortgage rates that will guarantee lost lending profits for years to come.

Meanwhile, on Friday, the Bank of Canada, recognizing the cratering impact of COVID-19 on the economy, lowered its benchmark interest rate to an almost nonexistent 0.25 percent, the third time in March it tried to come to the rescue by cutting the borrowing standard.

But even such a drastic move, lopping off 150 basis points in less than a month, might not be enough.

Bargain basement lending rates and mortgage deferral plans could be moot at a time when people can’t even venture outside. This week, the Ontario Real Estate Association told all agents to stop face-to-face business and shutdown all open houses.

Open House signs in Peel will not be seen this spring, for now

That might not be a big deal in an area of the province with low population growth, but in Brampton and Mississauga, where some 20,000 people arrive every year, any roadblock to acquiring housing could have serious consequences.

Meanwhile, for some who recently purchased, the timing couldn’t have been worse.

Annetta Ishmael, who lives in Mount Pleasant in Brampton, told The Pointer she was initially buoyed by finding out about the deferral program, only to have her hopes dashed. “I was laid off due to the current pandemic, so we explored deferring our Scotiabank mortgage,” she said. “[We] ultimately decided not to as our interest would accrue during the deferral period.”

On any mortgage, especially a relatively new one, an extra six months of interest being added to the total bill could lead to higher future payments or a longer payback time. The offer is, essentially, a solution to short-term cash flow issues with a long-term price tag.

Ishmael, who worked as a law clerk for a travel company until the pandemic, only recently moved into her new home. “It was a little devastating to get laid off since we just bought and furnished this house, this was a critical time for us to recoup our savings,” she added.

“The lay off was inevitable though, being in the tourism industry. I was a little disappointed to find out that after the deferral period my monthly payments would be higher. Because of the industry I work in I don't know that things will be back to business as usual in six months...we decided not to defer in case we aren't in a position to handle higher payments in the future.”

To add to the confusion and frustration homeowners like Ishmael are feeling in Peel, the information has been hard to find. The law clerk said calling the number provided by her bank only took her to a pre-recorded mail box, with the information she required buried in the frequently asked questions section of the website.

The issues experienced by Ishmael and others like her could soon be fixed, but there are no guarantees. On Thursday, a day before the Bank of Canada made its latest cut, Prime Minister Trudeau announced the federal government was in talks with banks, asking them to lower certain interest rates. Currently, some banks have lowered rates for existing floating-rate personal loans, and the PM wants to see credit card rate relief, but new loans and mortgage loans are a different story.

Banks are already swamped with hundreds of thousands of requests for mortgage payment deferrals, while the prospect of mass defaults on business loans and existing home mortgages amid widespread layoffs during this unprecedented economic stoppage has left the banks more exposed than ever, according to many economists.

Robert Hogue, an RBC senior economist, said even if borrowing rates are more attractive the uncertainty of COVID-19 is having a profound psychological impact, dissuading many who might otherwise want to make a real estate transaction.

"We are coming to the view now that because of the virus and the meltdown in financial markets, we will mostly likely see a decline in buying activity through at least parts of the spring market, and maybe even going into the summer market," he told the Financial Post last week.

For renters, the waters are muddier still.

In order to protect tenants who couldn’t afford rent, Ontario has suspended new evictions to offer peace of mind. In his daily press conferences, Premier Doug Ford has been vocal, repeatedly telling those who can’t afford rent simply not to pay. “No one will be kicked out of their home or their rental apartments based on not being able to pay the rent – it’s just not going to happen, we won’t allow it to happen,” Ford said last week.

“We’re going to get through this,” he added. “The landlords will get through it, but some people are going to face some tough times, but it doesn’t give a free pass to people just to say they aren’t paying – be responsible, pay if you can, but if you’re down and out and just don’t have the money, food is more important to put on the table than paying rent.”

So far, no legislative changes have been offered to enable this.

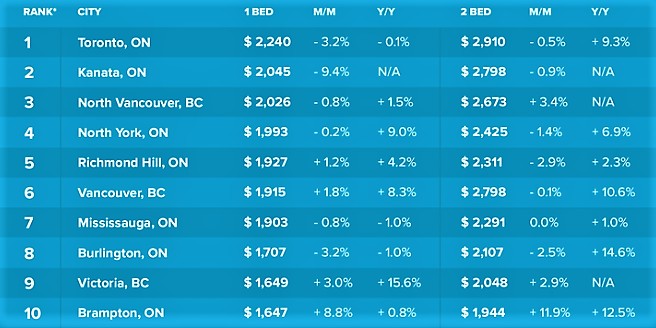

Canadian cities with the highest rental rates

The suspension of evictions without rent-specific measures and legislation raises a myriad of questions. It is unclear, for example, what is to stop landlords deceiving tenants into believing they face eviction, a particular problem in Mississauga and Brampton with tens of thousands of unregistered secondary units. Equally, will tenants who fail to pay run up a tab due immediately after the pandemic ends? Or, will landlords be forced to pass any property tax or utility savings onto their tenants?

The Pointer posed these questions to the province; the response offered no new details.

“It’s important to be clear that tenants must still pay rent as they normally would, to the best of their abilities, and that the rules of the Residential Tenancies Act still apply,” Conrad Spezowka, a spokesperson for the Government of Ontario, responded via email.

“We encourage landlords and tenants to work together during this difficult time to establish fair arrangements to preserve tenancies and sustain a healthy rental housing sector. We encourage tenants that are having challenges paying rent due to COVID-19 to speak with their landlords about possible deferral of rent payment or agreeing to other payment arrangements.”

He added that when the suspension on evictions is eventually lifted, “the landlord and the tenant will have the opportunity to provide evidence and arguments” at any eviction hearing.

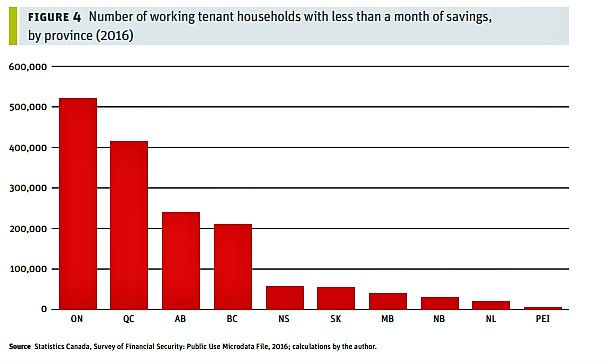

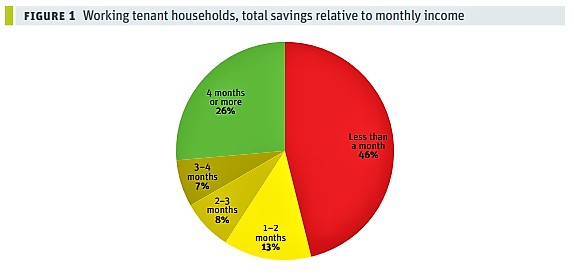

A 2016 study by the Canadian Centre for Policy Alternatives, found that 3.4 million Canadian households rent with wages or self-employment revenue, and 46 percent of households in this category had less than one month’s income in their savings. Of these, more than 500,000 were in Ontario.

Data from the United Way found that, in 2015, 60 percent of Brampton neighbourhoods were categorized as low income, with high rates of tenant housing catering to many in challenging financial circumstances.

Rental rates have since increased dramatically. The recent trend shows this continuing. According to Rentals.ca, the month-to-month rent average in the city increased by almost 12 percent in February, even as COVID-19 started to bring the national average down.

With April 1 the date most pay their landlord, and many facing financial uncertainty, Peel’s renters are waiting for answers.

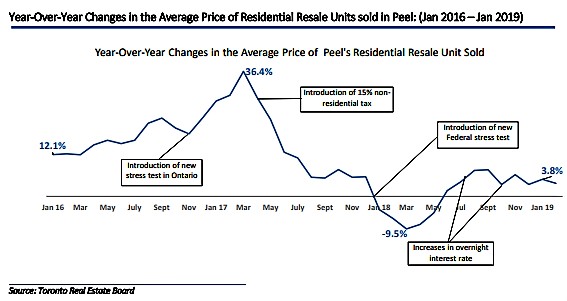

While it may offer little solace, the housing market tends to lag behind current events. The real estate industry is seeing the beginnings of what could be a drastic decline in sales.

For realtors in Mississauga and Brampton, the cash flow crisis, a confusing mortgage situation and a lack of certainty spell danger. Eddy Sousa, a realtor in Mississauga, told The Pointer he has had to end showings as a result of COVID-19.

“I have stopped showing homes, I'm not taking on clients and have decided to self isolate,” he said. “I'm finding many properties are being taken off the market, with the uncertainty of banking availability. We have stopped doing open houses [and are] focusing on virtual tours. [When I began self-isolating,] I had stopped driving people in my vehicle. Showings had become problematic since people didn't want strangers in their homes — [sellers] refused to open doors.”

Mississauga real estate agent Eddy Sousa

These worries were echoed by other realtors in the city, who fear physical distancing measures will temporarily hurt the market. Given the price of houses in both Mississauga and Brampton, few are likely to buy a home they’ve only seen in a video amid the ongoing pandemic.

As the crisis continues and residents struggle financially, the number of properties on the market could also increase, lowering prices due to oversupply. Ultimately, lower prices could be a disincentive for future development and construction across the region.

At least one economist does not think there will be a decline in house prices.

"The way I see it, the housing market is basically frozen — no buyers and no sellers. That, in a way, will limit or even eliminate any notable downward risk to prices,” Benjamin Tal, an economist at CIBC Capital Markets told Yahoo! Finance last week. “Simply, the number of sales will go down dramatically.”

In Peel, with its rapid population growth, the housing market has a delicate balance; extremely low vacancy rates mean there is no room for major changes. So, while a freeze might be fine for those who have housing, what happens to those actively looking for a home without any short-term accommodation lined up, or who have to vacate whatever housing they are currently in?

Another dilemma is what happens to new builds that need to be sold, often before construction has been completed, in order to meet financing obligations builders are constrained by.

Banks could be left holding the bag on projects that builders have to walk away from because of dried up cash flow as buyers suddenly disappear.

In order to sustain Peel’s projected growth, the region has calculated roughly 6,000 new units need to be built per year, alongside a healthy resale market. In 2018, the number of new starts in Peel fell to 4,978, something COVID-19 could dramatically exacerbate for 2020.

If the pandemic continues to bring the real estate market to a halt, scaring off potential buyers, Mississauga and Brampton will feel a knock-on effect. In the long run, the supply of new housing could begin to slow in response to lower demand (and more resales due to financial pressure), leaving even fewer housing options for residents in the future in a region with incredible pressure to keep growing.

Email: [email protected]

Twitter: @isaaccallan

Tel: 647 561-4879

Submit a correction about this story