Politically powerful seniors are staying in their homes, making it difficult to raise property taxes

The City of Mississauga might be 45-years-young, but not all of its residents are quite as sprightly. Although the city boasts a relatively young population, like so many municipalities in Canada, because of the boomer bulge, it has a rapidly growing senior demographic.

Of the three localities that make up the Region of Peel, Mississauga has the largest senior population, while Brampton has the lowest. Between 2001 and 2016 that population exploded, growing 124.4 percent. The 2016 numbers for Mississauga showed that residents 65 or older made up 22.3 percent of the population.

In the city and across the country, seniors present something of a conundrum, especially during budget season.

In the past, it was common for people to move house and downsize after retirement, with their reduced housing costs staying in line with decreased fixed incomes.

After children fled the nest, many parents would accept their pension, start drawing down on their retirement savings and move out of their detached house into something smaller and more manageable.

However, in recent years, that trend has reversed in tandem with the rapid growth of the senior demographic.

Research conducted during the summer by The Canada Mortgage and Housing Corporation shows that, over the past 10 years, residents in the GTA over the age of 65 have opted to remain in the real estate market. Where previously many would retire into supported housing or smaller rental units, or condos, seniors now make up 25 percent of local family-house owners in the Toronto Region, compared to 20 percent a decade ago.

Speaking to CBC during the summer, report author Inna Breidburg said that "Housing is a continuum, if seniors don't sell their homes, eventually it limits supply for all further generations ... It has implications for the entire market."

In Mississauga, where house prices have skyrocketed over the past few years, this is undoubtedly true.

There are a number of factors behind the trend. Improved healthcare and life expectancy mean that many senior residents are comfortable living in and maintaining a larger house well into their retirement, where previous generations chose to give it up. Equally, the incredibly heated GTA housing market means that property value continues to climb the longer it is owned, another incentive to keep it as a nest egg for as long possible. No one wants to walk away from an investment while it is rocketing upward.

In Peel, the region’s disastrous housing plan also means that the supply of affordable homes for seniors on a fixed income is just a fraction of the demand.

As The Pointer has previously reported, the region’s plan to add 75,000 new affordable housing units by 2028 is in disarray. The system’s waiting list sat at 14,997 in June, compared to 13,597 the same time last year, with many on the list waiting more than a decade for help. At its woeful current rate of adding to its supply, around two percent of its own annual target, the Region of Peel will not achieve its affordable housing target until the year 2547.

New affordable housing units constructed in Malton

This situation, where circumstance and preference has led to far fewer seniors choosing to downsize, presents a problem for municipalities.

It’s thrust to the forefront during budget season in particular, when seniors on fixed incomes (the most powerful voters in the city) stand to oppose property tax increases.

Statistics compiled by the City of Guelph, which had a similar voter turnout rate for last year’s municipal election compared to Mississauga, show just how powerful the senior vote is at the local level.

In the 2018 municipal election, 50 percent of eligible voters in Guelph aged 60 to 79 cast a ballot, compared to 26 percent of those aged 22 to 39. So, this means people nearing or in retirement vote at twice the rate compared to those in their early 20s to their late 30s.

And this means that municipal decision making by elected council members, especially during budget season, will most likely cater to the voters who matter the most to those thinking about holding onto their jobs in the next election.

Seniors and other residents filled Mississauga's council chamber early in the year to show support for the city's exit from Peel Region

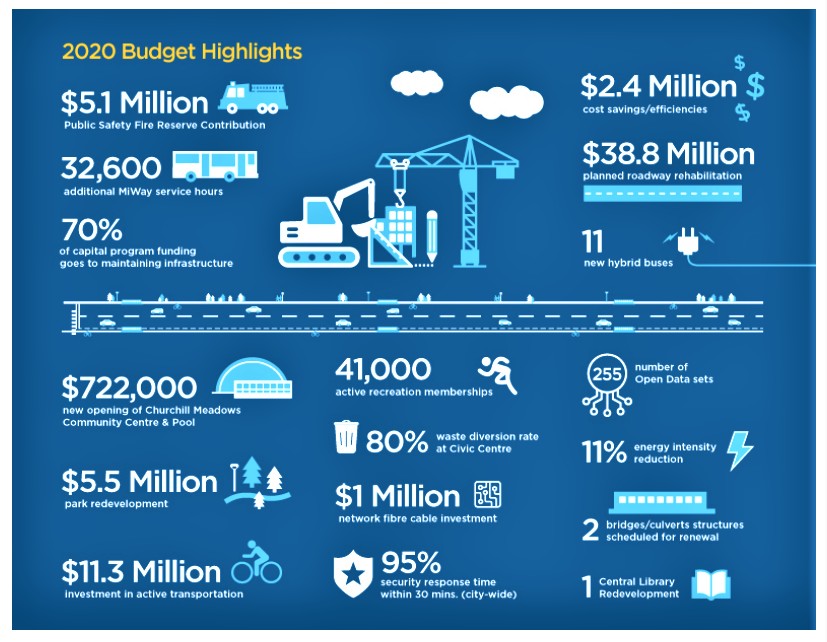

On paper seniors represent one of the better off segments of society due to the value of assets acquired over time, yet fixed retirement incomes are often lower than average wages and sometimes even below the poverty line. It’s a dilemma for those in retirement who choose to hang onto their expensive homes. As a result, in Mississauga, several councillors including Ron Starr and Dipika Damerla, raised the issue of squeezing seniors when referencing the city’s proposed 4.9 percent budget increase, which would be reflected in its share of the 2020 property tax bill (this does not include the city’s stormwater charge, the Region of Peel’s proposed net tax levy increase of 4.3 percent on its share of the property bill or the region’s proposed 6.3 percent utility rate increase for 2020).

The dilemma: keep taxes low or pay for what the city needs

These numbers for 2020, which, if approved by city and regional council, come in far above inflation, with the proposed tax and utility rate increases for homeowners in 2020 hovering at triple the current rate of increase they pay in Ontario for most consumer items and services.

Such dramatic cost increases for municipal services have a particularly harsh impact on seniors.

Alongside a natural compassion for those on fixed incomes, seniors are a powerful and motivated voting bloc.

In Mississauga in particular, where a Hazel McCallion monopoly on political power for decades bred glaringly low election turnouts, the financial reality is even more of a dilemma for council members.

The city is in dire need of more revenue to keep up with the costs of growth, but how can it pay for things such as better transit coverage, if fixed-income seniors, who are the most powerful voting bloc, demand low property taxes.

Local elected officials now face a decision: pass a budget with increases the city desperately needs; or listen to the voters who matter the most and find ways to cut.

In the most recent election last year, a turnout below 30 percent showed the depths of disengagement in the city. When disengagement is low, national statistics suggest seniors are more likely to make up an even larger share of the vote. Numbers from the 2011 federal election put the turnout of 65 to 74-year-old voters at 75.1 percent, compared to 38.8 percent of 18 to 24-year-olds. Even in 2015, where a wave of young, first-timer voter enthusiasm swept Justin Trudeau to power, 78.8 percent of those aged 65 to 74 voted compared to 57.1 percent of 18 to 24-year-olds.

Such data is not available for most municipal elections, however the results in Guelph last year illustrate the power of the senior vote. These same seniors, many of whom are on fixed incomes, live in valuable homes and would have a more difficult time managing property tax increases that far outstrip their income gains.

In 2019 the average home in Mississauga has an assessed value of 688,000 and property owners pay about $4,900 in taxes on this amount. This does not include the stormwater charge and all the utility fees. At approximately $5,800 for all these combined (this is an estimate for an average Mississauga home), the figure represents a large share of the average after-tax household income for couples in Mississauga living without children. According to the last census this amount stood at $70,835 in 2015.

In Mississauga, a generally young city with a large portion of families who moved here to buy their first home, these statistics point to a range of issues.

For seniors who have chosen to remain in larger family homes in their retirement, the tax burden is a real issue. This issue is something which weighs heavily on councillors minds as, ultimately, seniors represent a much larger share of the vote count. Meanwhile, this pours petrol on the already torridly heated housing market by choking off a significant part of the supply. Seniors and the environment both suffer as they have to spend money on energy to heat and cool homes larger than they need; money taken from a fixed income that can’t keep up with costs such as property taxes.

The scenario might not engender much sympathy for those who buck the traditional trend and choose to stay in their large family home long after retirement, but it is a reality.

The solution seems simple: when you retire, find a new home and put some of the profit of selling toward renting or buying a more affordable unit.

However, it’s not that simple. One of the positives of seniors holding onto their homes is a rise in the benefits of “aging in place”, the physical and emotional advantages of living where one is most happy and comfortable, and the creation of mixed communities in terms of the value of providing services.

For city-run services such as libraries or those which can command fees, such as community centres or fitness spaces, retired individuals are generally more likely to have the time and resources to utilize these key municipal features.

Many choose to “age in place” to stay close to their families and remain part of the communities in which they have made friends and built relationships. Forcing seniors to move out of their homes and search several miles away for suitable supported rental spaces or alternative independent living options would do little to combat age-related emotional and physical degeneration, while essentially creating ghettos of isolated residents less mobile than the average resident. Many seniors are extremely productive, contributing to their communities through volunteer participation, political engagement and even working at part-time jobs. Some even work full time into their 70s and beyond; the city's legendary former mayor, who turns 99 on Valentine's Day, being the perfect example.

So what can Mississauga do about this growing trend?

A combination of development planning for smaller, accessible units interspersed through the city’s existing neighbourhoods and a regional housing plan that works are key.

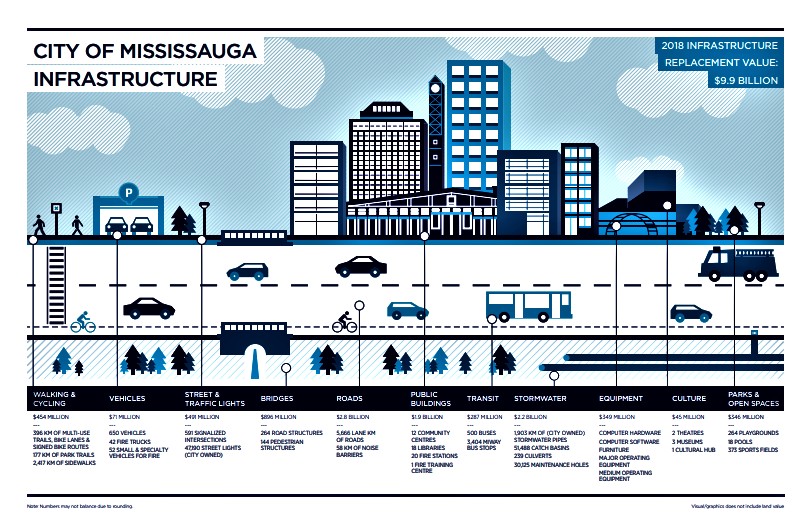

Would it be too radical to propose tax and utility-fee breaks for those 65 and older, considering they likely do not use large portions of the municipal infrastructure as much, for example, the costly road and transportation network that accounts for almost $4.2 billion of the city’s $9.9 billion in overall assets?

This sort of equalization is controversial and complicated, as a larger share of the overall budgetary burden would have to be covered by younger property tax payers. But if they are the ones using the lion’s share of the city’s infrastructure, and will benefit well into the future from current investments paid for through the property tax, shouldn’t they pay a larger share for what they more frequently use?

It was a similar, progressive, philosophy that drove the city to change its approach to stormwater fees, when a few years ago it adopted a charge based on the size of each property. Now, the amount is based on how much water it sends into the storm infrastructure so owners of larger homes that cover more land, not allowing rain water to absorb into the ground, pay more than owners of smaller properties, instead of having fixed rates.

Possible resentment from younger people frozen out of the housing market by seniors holding onto their homes or lower tax policies to appease retirees, might be misplaced. It’s unreasonable to expect anyone who is happy and healthy to uproot to a totally new living arrangement for the good of market supply.

For now, City Council will have to walk a fine line between a tax increase that adequately funds the voracious needs of a young, dynamic city, and appeasing older, powerful voting blocs with a unique set of concerns.

Email: [email protected]

Twitter: @isaaccallan

Submit a correction about this story